Internal Revenue Code Section 199A provides a potent mechanism for reducing the effective tax rate applied to ordinary income generated by pass-through entities. The statutorily defined Qualified Business Income (QBI) deduction allows eligible non-corporate taxpayers to deduct up to twenty percent of their qualified business income, effectively shielding a fifth of business profits from top-tier marginal rates. The Working Families Tax Cut Act permanently extends the operational lifespan of Section 199A, which was originally scheduled to sunset at the conclusion of the 2025 taxable year, thereby securing this vital deduction through 2029.

The calculation and application of the QBI deduction are governed by highly complex limitations based on the taxpayer’s overall taxable income. These limitations primarily consist of the W-2 wage and Unadjusted Basis Immediately after Acquisition (UBIA) of qualified property tests, as well as the outright exclusion of income derived from Specified Service Trades or Businesses (SSTBs). The definition of an SSTB is particularly critical for the entertainment industry, as it explicitly encompasses businesses operating in the fields of performing arts, consulting, athletics, and any trade where the principal asset is the reputation or skill of one or more of its employees or owners. Consequently, talent agencies, individual performers structured as loan-out S-Corporations, and specialized management firms are overwhelmingly classified as SSTBs.

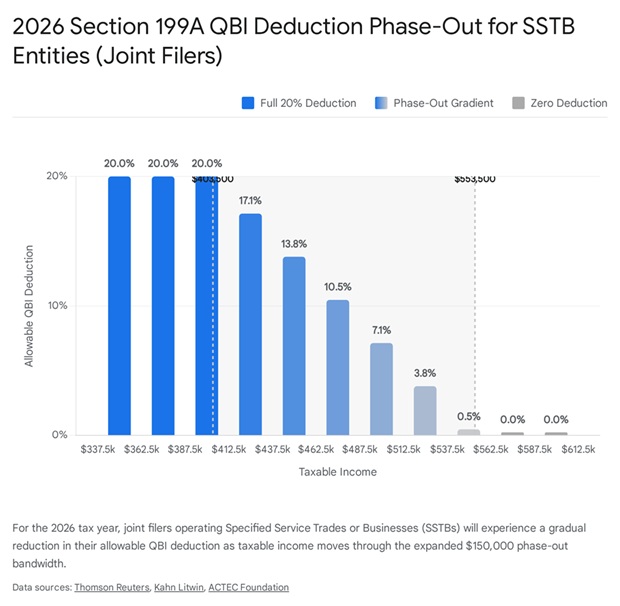

When a taxpayer’s taxable income exceeds defined thresholds, the QBI deduction for SSTBs is subject to a strict phase-out, ultimately resulting in the complete disallowance of the deduction once the income exceeds the phase-out bandwidth. For non-SSTB pass-through entities (such as equipment rental firms, physical production studios, or property holding LLCs), exceeding the threshold subjects the deduction to the W-2 wage and UBIA limitations rather than an absolute phase-out.

The legislative amendments introduce significant, taxpayer-favorable expansions to these phase-in ranges beginning in the 2026 taxable year. Prior to these adjustments, the phase-in range spanned a bandwidth of $100,000 for married couples filing jointly and $50,000 for all other filers. For 2026, the legislation expands the phase-in bandwidth to $150,000 for joint filers and $75,000 for single and head of household filers.

Mathematically, the base income threshold at which the phase-in process commences has also been heavily adjusted for inflation. For the 2026 taxable year, the phase-in range for joint filers begins at $403,500 and completely phases out at $553,500 (up from the 2025 parameters of $394,600 to $494,600). For single individuals and heads of households, the 2026 phase-in range is bounded between $201,750 and $276,750.

Furthermore, the legislation establishes a new minimum QBI deduction to simplify calculations for smaller enterprises. Starting in 2026, a taxpayer reporting a minimum of $1,000 in total QBI from an active qualified trade or business is statutorily entitled to claim a minimum QBI deduction of $400, irrespective of other overarching limitations.

| 2026 Section 199A Thresholds | Single / Head of Household | Married Filing Jointly |

| Phase-in Range Start | $201,750 | $403,500 |

| Phase-in Range End | $276,750 | $553,500 |

| Total Phase-out Bandwidth | $75,000 | $150,000 |

For S-Corporation proprietors, the interaction between reasonable compensation (W-2 wages paid to the shareholder-employee) and the QBI deduction demands precise calibration. W-2 wages inherently reduce the net QBI eligible for the 20% multiplier, yet they are simultaneously required to satisfy the wage limitation tests for taxpayers exceeding the income thresholds. With the phase-in ranges expanding to $553,500 for joint filers in 2026, many S-Corporation owners who were previously locked out of the deduction may now find themselves within the phase-in bandwidth. This necessitates a total recalculation of optimal payroll distributions versus pass-through profit taking. Strict adherence to documentation standards regarding trade or business classifications is mandatory to support positions taken upon subsequent IRS or FTB audit.