The engagement and compensation of independent contractors form the operational backbone of the modern entertainment and media production industries. Corporations, Limited Liability Companies, and individual producers routinely disburse nonemployee compensation to vast networks of specialized personnel, ranging from set designers, lighting technicians, and acoustic engineers to independent creative talent and post-production consultants. Historically, the Internal Revenue Service has enforced a rigid and low-bar information reporting threshold, mandating that payors issue Form 1099-NEC (Nonemployee Compensation) or Form 1099-MISC (Miscellaneous Information) for any aggregate payments to a single payee equaling or exceeding $600 within a calendar year.

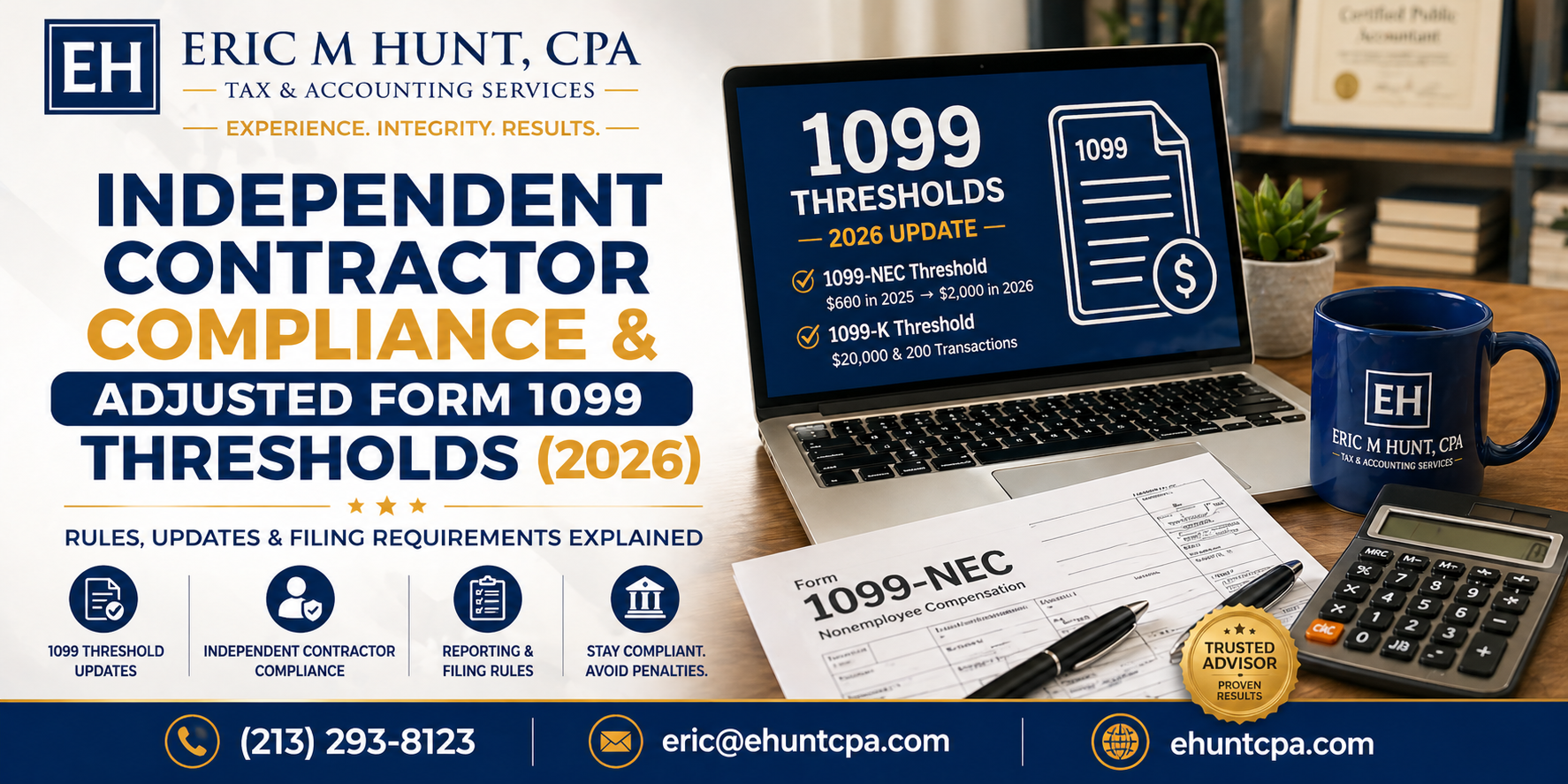

Section 70433 of the Working Families Tax Cut Act institutes a comprehensive structural reform of these reporting obligations. Effective for taxable years beginning after December 31, 2025, the statutory threshold for generating and filing Forms 1099-NEC and 1099-MISC is drastically increased from the legacy $600 baseline to a new threshold of $2,000. Furthermore, ensuring that this threshold does not erode over time, the $2,000 figure will be subjected to annual inflation adjustments commencing in the 2027 calendar year.

This legislative adjustment represents a profound reduction in administrative overhead and compliance burdens for payor entities. The sheer volume of information returns requiring accounting processing, printing, and secure digital transmission to the IRS will decrease substantially. Concurrently, the legislation dictates that third-party network transaction reporting requirements, administered via Form 1099-K (utilized by payment processors and merchant acquiring entities), will repeal the temporary $600 limit set by the American Rescue Plan Act of 2021 and revert to the original, more lenient threshold of $20,000 in aggregate payments accompanied by a minimum of 200 distinct transactions.

Despite the operational relief provided by the elevated $2,000 threshold, strict adherence to compliance protocols remains mandatory. It is critical to recognize that while payments falling below the $2,000 threshold are exempt from mandatory 1099 reporting by the payor, these amounts still constitute fully taxable income for the payee and must be reported on their respective individual tax returns.

Moreover, the statutory requirements governing backup withholding have been similarly modified. Effective 2027, payors are obligated to initiate backup withholding only when aggregate calendar year payments exceed the inflation-adjusted $2,000 threshold and the payee has failed to supply a valid Taxpayer Identification Number (TIN) via an authorized Form W-9.8 To ensure continuous compliance and insulate the enterprise from severe civil penalties associated with failure to file, businesses must maintain rigorous vendor onboarding procedures. The collection of a duly executed Form W-9 prior to the disbursement of any initial funds must remain an unalterable corporate policy, regardless of whether the anticipated compensation volume will eclipse the new $2,000 threshold.

Internal accounting platforms, accounts payable software architectures, and automated vendor management systems must be reconfigured prior to January 1, 2026, to recognize the $2,000 trigger point and suppress the erroneous generation of information returns for sub-threshold vendors. Proactive preparation is required to prevent misreporting and unnecessary compliance costs in the upcoming filing seasons.