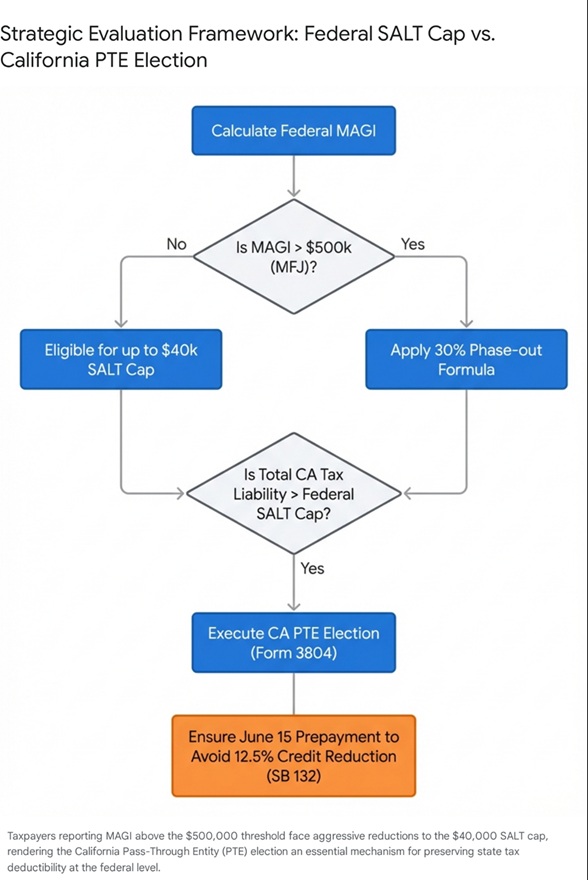

The enactment of the Working Families Tax Cut Act has fundamentally altered the landscape of itemized deductions by elevating the federal State and Local Tax (SALT) deduction cap from $10,000 to $40,000 for the 2025 through 2029 tax periods. However, the application of this expanded cap is not absolute and contains inherent traps for unwary taxpayers. The statutory framework subjects high-net-worth taxpayers to an aggressive phase-out mechanism designed to recapture the benefit. For married individuals filing jointly, the $40,000 limitation is reduced by thirty percent of the amount by which their Modified Adjusted Gross Income (MAGI) exceeds $500,000. This phase-out mathematically dictates that joint filers with a MAGI reaching $600,000 will see their SALT cap revert precisely to the baseline floor of $10,000, neutralizing the intended benefit of the legislation.

For taxpayers domiciled in California, particularly those generating substantial revenue through S-Corporations or partnerships within the highly compensated entertainment sector, state tax liabilities invariably surpass these federal limitations, regardless of whether the cap sits at $10,000 or $40,000. Consequently, the California Pass-Through Entity (PTE) elective tax – originally enacted under Assembly Bill 150 and refined by Assembly Bill 87 – remains an indispensable instrument for tax architecture. The recent passage of California Senate Bill 132 (SB 132) ensures the continuity of this program by extending the PTE election availability through the 2030 taxable year, decoupling California’s strategy from the federal 2029 sunset provisions.

The PTE elective tax functions as a legally sanctioned workaround to the federal SALT cap limitation. By electing to remit a 9.3% tax on qualified net income at the entity level, the pass-through entity secures a fully deductible federal business expense, thereby reducing the distributive share of federal taxable income passed through to the respective owners. Concurrently, the individual owners receive a non-refundable California income tax credit equal to the amount of tax paid by the entity, effectively preventing double taxation at the state level while preserving the federal deduction.

Senate Bill 132 introduces critical procedural modifications effective for taxable years beginning on or after January 1, 2026. Under prior law, the failure to remit a mandatory prepayment by June 15 – calculated strictly as the greater of $1,000 or fifty percent of the prior year’s PTE tax liability – resulted in the irrevocable invalidation of the PTE election for that entire taxable year. The revised statute under SB 132 provides a vital, though punitive, safe harbor: an insufficient or entirely omitted June 15 prepayment no longer disqualifies the entity from making the election. Instead, the legislation imposes a statutory penalty in the form of a 12.5% reduction to the allowable credit applied directly against the exact amount of the prepayment shortfall.

| PTE Tax Parameter | Pre-SB 132 (Through 2025) | Post-SB 132 (2026 – 2030) |

| Election Deadline | Businesses must make election payments by June 15 or lose the election. | No payment is required to elect, but credit may be reduced. |

| June 15 Prepayment | Required: Greater of $1,000 or 50% of prior-year PTET. | Recommended: Same amount to avoid credit reduction. |

| Penalty for Missing Prepayment | Strategy not possible (Election Invalidated). | Strategy possible, but tax credit reduced by 12.5% of the unpaid June 15 prepayment amount. |

| Final PTET Payment | December 31 of the same tax year. | December 31 of the same tax year. |

Therefore, to maximize the allowable credit and preserve the highest tier of federal deductibility, it is imperative that all qualifying entities meticulously calculate and process the required June 15 prepayment. The strategic interaction between the federal SALT cap phasedown and the California PTE election dictates that virtually all S-Corporations and partnerships generating significant net income must continue to execute the PTE election.

Taxpayers must ensure that all entity-level financial projections are updated to account for the inflation-adjusted 2026 federal phase-out threshold, which increases from $500,000 to $505,000 for joint filers. Furthermore, for the 2027 tax year, this threshold will increase again to $510,050. The failure to coordinate federal MAGI calculations with state-level PTE estimated payments will result in suboptimal tax positioning.