This guide explains the tax consequences associated with Intellectual Property (IP). It establishes the foundational concepts outlined in the 2013 AICPA framework and provides an authoritative update on current 2024/2025 tax laws, specifically addressing the implications of the Tax Cuts and Jobs Act (TCJA) and corporate IP worthlessness scenarios under IRC § 165 and § 197.

1. Foundational Rules (AICPA Baseline)

Context & Purpose

The section below outlines the historical and foundational tax principles for individuals creating intellectual property, as detailed in the 2013 AICPA report. It distinguishes between royalties and compensation, outlines deductible business costs, and defines the criteria for treating an IP transfer as a sale versus a license. Click on the cards to review the formal parameters of each category.

💰 Income Classification – Royalties vs. Compensation

Amounts received by individuals who create IP may be classified as royalties or compensation. This classification depends on whether the individual owns and licenses the property (Royalties) or creates it as a work-for-hire for an employer (Compensation). Royalties may further be classified as business or nonbusiness income depending on the taxpayer’s trade or business status.

📈 Deductions & Costs – Business Expenses & Capitalization

Individuals engaged in the trade or business of creating intellectual property may deduct ordinary and necessary business expenses under IRC § 162. Furthermore, certain creative expenses are exempt from the uniform capitalization (UNICAP) rules of IRC § 263A, allowing for immediate deduction of qualified creative costs rather than capitalizing them into the basis of the asset.

📝 IP Transfers – Sale vs Licensing Agreements

The tax treatment of an IP transfer hinges on whether “all substantial rights” to the property have been transferred. A transfer of all substantial rights is generally treated as a sale. Conversely, retaining substantial rights (such as geographic or temporal limitations) typically categorizes the transaction as a license.

🎁 Gifts & Bequests – Estate & Gift Tax Implications

Similar to direct transfers, the terms of a bequest or gift of intellectual property dictate whether all substantial property rights have been transferred. This determination controls how the bequest or gift is treated for estate, gift, and subsequent income tax purposes for the beneficiary.

2. Current Law Updates (TCJA)

Have the Rules Changed Since 2013?

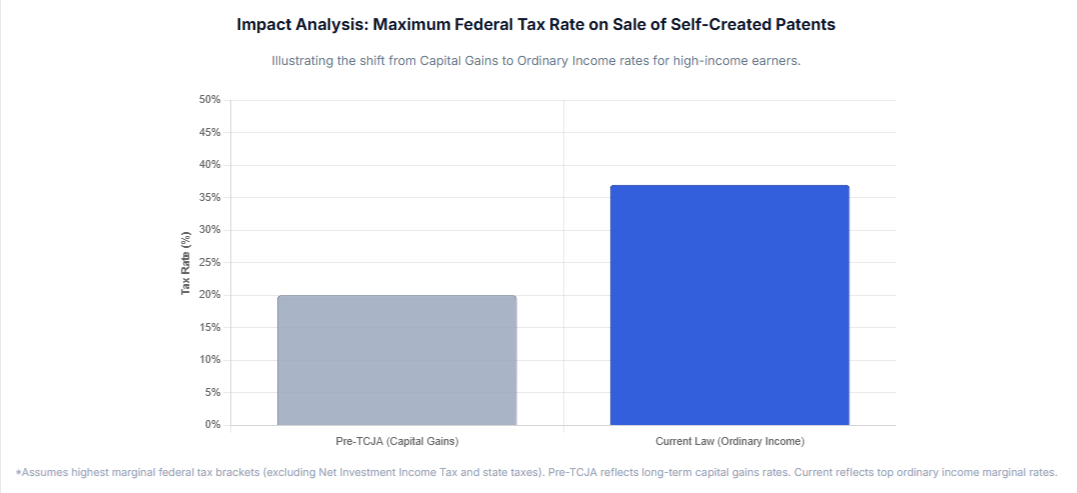

Yes. The tax rules relating to the tax consequences of self-created Intellectual Property have changed significantly compared to the 2013 analysis.

The primary catalyst for this change was the Tax Cuts and Jobs Act (TCJA) of 2017. Prior to the TCJA, creators of patents, inventions, models, and designs could often achieve favorable long-term capital gains treatment upon the sale or exchange of their intellectual property. The current law has fundamentally altered this treatment.

Current Treatment of Self-Created IP

Under current law (specifically amended IRC § 1221(a)(3)), self-created patents, inventions, models, designs, secret formulas, and processes are explicitly excluded from the definition of a capital asset. Consequently, the sale or exchange of these self-created assets by the creator generally results in ordinary income, aligning their treatment with copyrights, literary, musical, or artistic compositions.

3. Corporate IP Worthlessness (2025)

Corporate IP Worthlessness in 2025

When a U.S. company purchases intellectual property, and it subsequently becomes entirely worthless, the tax treatment of the resulting loss depends heavily on how the asset was acquired. Use the guide below to determine the appropriate tax treatment under current 2025 regulations.

Worthless IP Loss Characterization

Did the U.S. company purchase the IP as a standalone asset, or was it acquired alongside other intangible assets (e.g., in an acquisition of a trade or business)?

Purchased Alone (Standalone)

✓ Ordinary Loss (IRC § 165)

If the IP becomes entirely worthless in 2025 and is formally abandoned, the loss is an ordinary loss under IRC § 165.

Explanation: Because the asset is deemed worthless and abandoned, there is no “sale or exchange.” A sale or exchange is a requisite statutory element for a capital loss. Without it, the loss on a business asset defaults to an ordinary loss, fully deductible against ordinary income in the year of abandonment.

Purchased with Other Intangibles

⚠️ Loss Disallowed (IRC § 197(f)(1))

If the IP was acquired in a transaction with other Section 197 intangibles (e.g., goodwill, customer lists) and the other intangibles are retained, no loss is recognized upon the worthlessness of the single IP asset.

Explanation: Under the special disposition rules of IRC § 197(f)(1), a taxpayer cannot recognize a loss on the disposition or worthlessness of a Section 197 intangible if the taxpayer retains other Section 197 intangibles acquired in the same transaction. Instead, the adjusted basis of the worthless IP is allocated to, and increases the basis of, the retained intangibles, continuing to amortize over the remainder of the 15-year period.

If you have any questions or require further documentation regarding the matters discussed in this guide, please contact our office. Thank you for your business!

Circular 230 Disclosure: Any tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.